Free Employee Loan Agreement Template

Things You Should Know About This Form

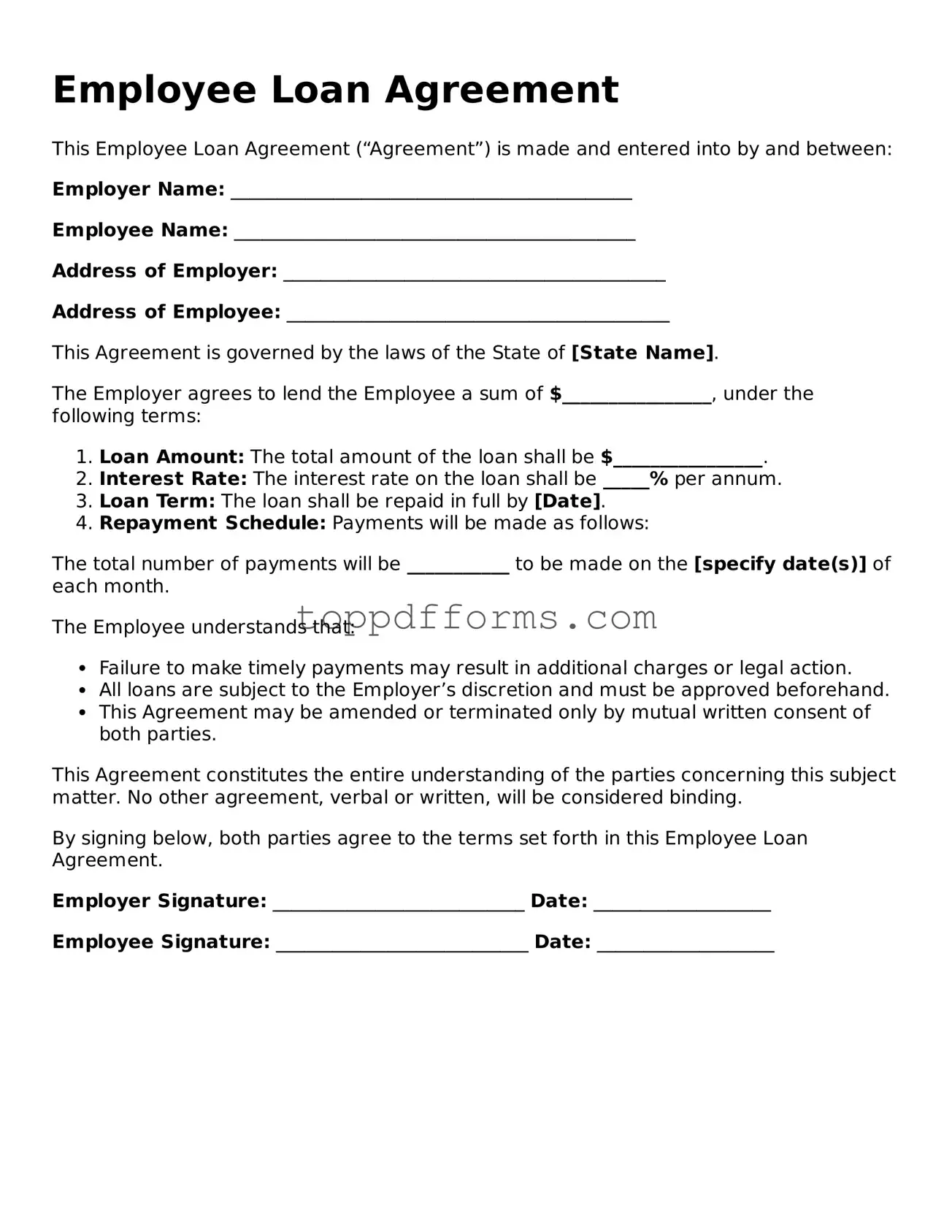

What is an Employee Loan Agreement form?

An Employee Loan Agreement form is a document that outlines the terms and conditions under which an employer provides a loan to an employee. This agreement typically includes details such as the loan amount, interest rate, repayment schedule, and any penalties for late payments. It serves to protect both parties by clearly defining their responsibilities and expectations regarding the loan.

Who is eligible to apply for a loan under this agreement?

Generally, any employee who has been with the company for a certain period and meets specific criteria can apply for a loan. Eligibility requirements may vary by organization, but they often include factors like employment status, length of service, and financial need. It’s important to check with your HR department for the specific guidelines applicable to your workplace.

What happens if I cannot repay the loan on time?

If you find yourself unable to repay the loan according to the agreed-upon schedule, it’s crucial to communicate with your employer as soon as possible. Many organizations have policies in place to address such situations, which may include restructuring the payment plan or discussing potential penalties. Open communication can help avoid misunderstandings and find a workable solution.

Can I use the loan for any purpose?

Is the loan amount taxable?

In most cases, loans provided by an employer are not considered taxable income, as long as the loan is structured correctly and repaid according to the terms. However, if the loan is forgiven or not repaid, it may be treated as income and subject to taxation. Always consult a tax professional for personalized advice regarding your specific situation and obligations.

PDF Overview

| Fact Name | Details |

|---|---|

| Purpose | An Employee Loan Agreement outlines the terms under which an employer lends money to an employee. |

| Repayment Terms | The agreement specifies how and when the employee must repay the loan, including interest rates if applicable. |

| Governing Law | The agreement is typically governed by the laws of the state where the employer is located. |

| Confidentiality | Both parties may agree to keep the terms of the loan confidential, protecting sensitive information. |

| Default Conditions | The form outlines what happens if the employee fails to repay the loan, including potential consequences. |

| Signatures Required | Both the employer and employee must sign the agreement to make it legally binding. |

Common mistakes

When filling out an Employee Loan Agreement form, clarity and accuracy are paramount. One common mistake is failing to provide complete personal information. This includes the employee's full name, address, and contact details. Incomplete information can lead to confusion and delays in processing the loan.

Another frequent error is neglecting to specify the loan amount. It's essential to clearly state how much money is being borrowed. If this detail is missing, the agreement may be considered invalid or unenforceable.

People often overlook the importance of detailing the repayment terms. This includes the repayment schedule, interest rate, and any penalties for late payments. Without these terms clearly outlined, misunderstandings can arise, potentially leading to disputes.

Some individuals forget to include the purpose of the loan. Stating the reason for borrowing can help clarify the agreement's intent and may be necessary for record-keeping purposes.

Another mistake is not having the agreement signed by both parties. An unsigned document may not hold up in a legal context. Both the employer and employee should sign the agreement to confirm their understanding and acceptance of the terms.

People may also fail to keep a copy of the signed agreement. It is vital for both parties to retain a copy for their records. This can help avoid future misunderstandings about the loan's terms.

Some employees neglect to read the entire agreement before signing. This can lead to agreeing to terms that are not fully understood. Taking the time to review the document can prevent complications down the line.

Inaccurate dates are another common issue. The date of the agreement and the repayment start date must be correct. Errors in dates can lead to confusion regarding when payments are due.

Additionally, not consulting with a financial advisor or legal professional can be a mistake. Seeking advice can provide clarity on the implications of the loan and ensure that both parties are protected.

Finally, people sometimes assume that verbal agreements are sufficient. Relying on oral promises can lead to significant problems later. A written agreement is crucial for establishing clear expectations and protecting both parties' interests.