Loan Agreement Document for Florida State

Things You Should Know About This Form

What is a Florida Loan Agreement form?

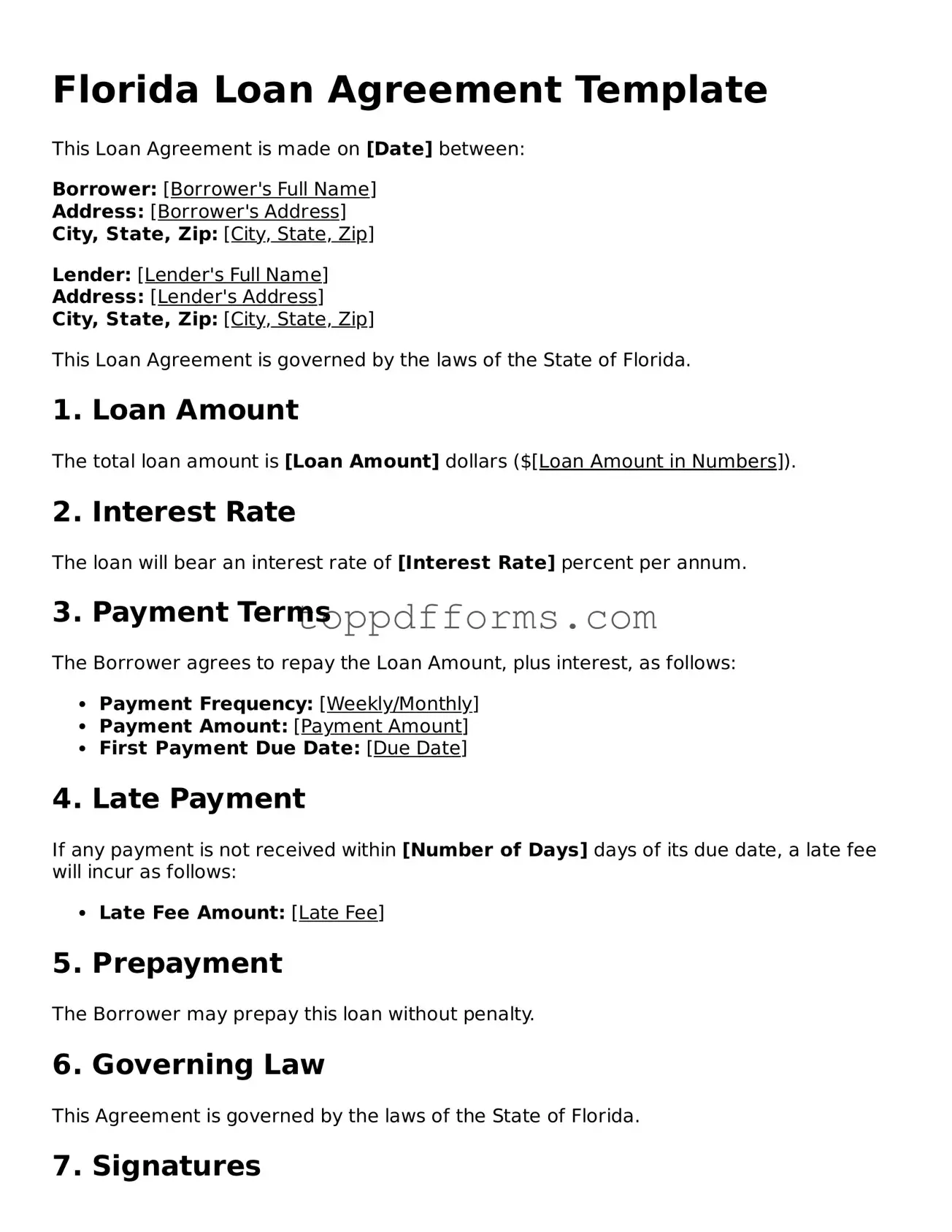

A Florida Loan Agreement form is a legal document that outlines the terms and conditions of a loan between a lender and a borrower in Florida. It specifies details such as the loan amount, interest rate, repayment schedule, and any collateral involved. This form helps protect both parties by clearly stating their rights and obligations.

Who can use a Florida Loan Agreement form?

Anyone who is lending or borrowing money in Florida can use this form. This includes individuals, businesses, and organizations. It's important for both parties to understand the terms of the agreement before signing to ensure that all expectations are clear.

What are the key components of a Florida Loan Agreement?

The key components typically include the names and contact information of both the lender and borrower, the loan amount, interest rate, repayment terms, and any fees. Additionally, it may outline what happens in case of default, such as late fees or legal actions.

Is the Florida Loan Agreement form legally binding?

Yes, once both parties sign the Florida Loan Agreement, it becomes a legally binding contract. This means that both the lender and borrower are obligated to follow the terms outlined in the agreement. If either party fails to comply, the other party may have legal recourse.

Do I need a lawyer to create a Florida Loan Agreement?

While it's not required to have a lawyer to create a Florida Loan Agreement, consulting one can be beneficial. A lawyer can help ensure that the agreement complies with state laws and adequately protects your interests. However, many people successfully create their own agreements using templates or online resources.

Can the terms of a Florida Loan Agreement be modified?

Yes, the terms of a Florida Loan Agreement can be modified if both parties agree to the changes. It’s important to document any modifications in writing and have both parties sign the updated agreement. This helps prevent misunderstandings in the future.

What should I do if a borrower defaults on the loan?

If a borrower defaults, the lender should first review the terms of the Loan Agreement to understand their options. This may include sending a formal notice of default or initiating legal proceedings. It’s often advisable to consult with a legal professional to explore the best course of action.

PDF Overview

| Fact Name | Details |

|---|---|

| Definition | The Florida Loan Agreement form is a legal document outlining the terms of a loan between a lender and a borrower in Florida. |

| Governing Law | This agreement is governed by the laws of the State of Florida, specifically Florida Statutes Chapter 687. |

| Parties Involved | The form typically includes the names and contact information of both the lender and the borrower. |

| Loan Amount | The specific amount of money being loaned is clearly stated in the agreement. |

| Interest Rate | The agreement specifies the interest rate, which can be fixed or variable, applicable to the loan. |

| Repayment Terms | Details regarding the repayment schedule, including due dates and payment methods, are outlined. |

| Default Consequences | The form includes provisions that describe the consequences if the borrower defaults on the loan. |

Common mistakes

Filling out the Florida Loan Agreement form is a critical step in securing a loan. However, many individuals make common mistakes that can lead to complications down the line. One prevalent error is failing to provide complete personal information. This includes not just names and addresses but also social security numbers and contact details. Incomplete information can delay processing and may even lead to the rejection of the application.

Another frequent mistake is neglecting to read the terms and conditions thoroughly. Borrowers often skim through the document, missing crucial details regarding interest rates, repayment schedules, and penalties for late payments. Understanding these terms is essential for making informed decisions and avoiding potential financial pitfalls.

Additionally, many applicants underestimate the importance of accurate financial disclosures. When individuals provide incorrect income or asset information, it can raise red flags for lenders. This misrepresentation, whether intentional or accidental, can jeopardize the loan approval process.

Another mistake involves not including all necessary documentation. Lenders typically require proof of income, bank statements, and other financial documents. Omitting these can lead to delays or denials. It is vital to double-check that all requested documents are included before submission.

Some borrowers also fail to sign the agreement properly. This may seem trivial, but missing signatures can invalidate the agreement. Each required signature must be present, and any changes made to the document should be initialed to avoid confusion.

Misunderstanding the loan amount is another issue that often arises. Borrowers may request more money than they need or less than what they qualify for. It is important to assess financial needs accurately and align them with what lenders are willing to provide.

Moreover, many individuals overlook the importance of understanding their credit score. A low credit score can significantly impact loan terms, including interest rates. Before filling out the form, reviewing your credit history can help you prepare for discussions with lenders.

Finally, failing to ask questions is a common oversight. If any part of the agreement is unclear, seeking clarification from the lender is crucial. Ignoring uncertainties can lead to misunderstandings and unfavorable loan conditions. Taking the time to ask questions can save borrowers from future headaches.

Other Common State-specific Loan Agreement Forms

Promissory Note Template Illinois - Borrowers should understand the implications of agreeing to the terms outlined in the Loan Agreement.

Texas Promissory Note Requirements - Potential changes in loan terms should be documented and agreed upon by both sides.

When dealing with real estate transactions, particularly those involving a Texas Quitclaim Deed, it's crucial to ensure that all parties understand the implications of the transfer. This form facilitates the ownership change without guaranteeing the title's quality, making it ideal for informal transfers. For those looking for reliable templates to guide them through the process, PDF Templates can be an invaluable resource.

Sample Promissory Note California - Loan agreements may include co-signer requirements for additional security.