Promissory Note Document for Florida State

Things You Should Know About This Form

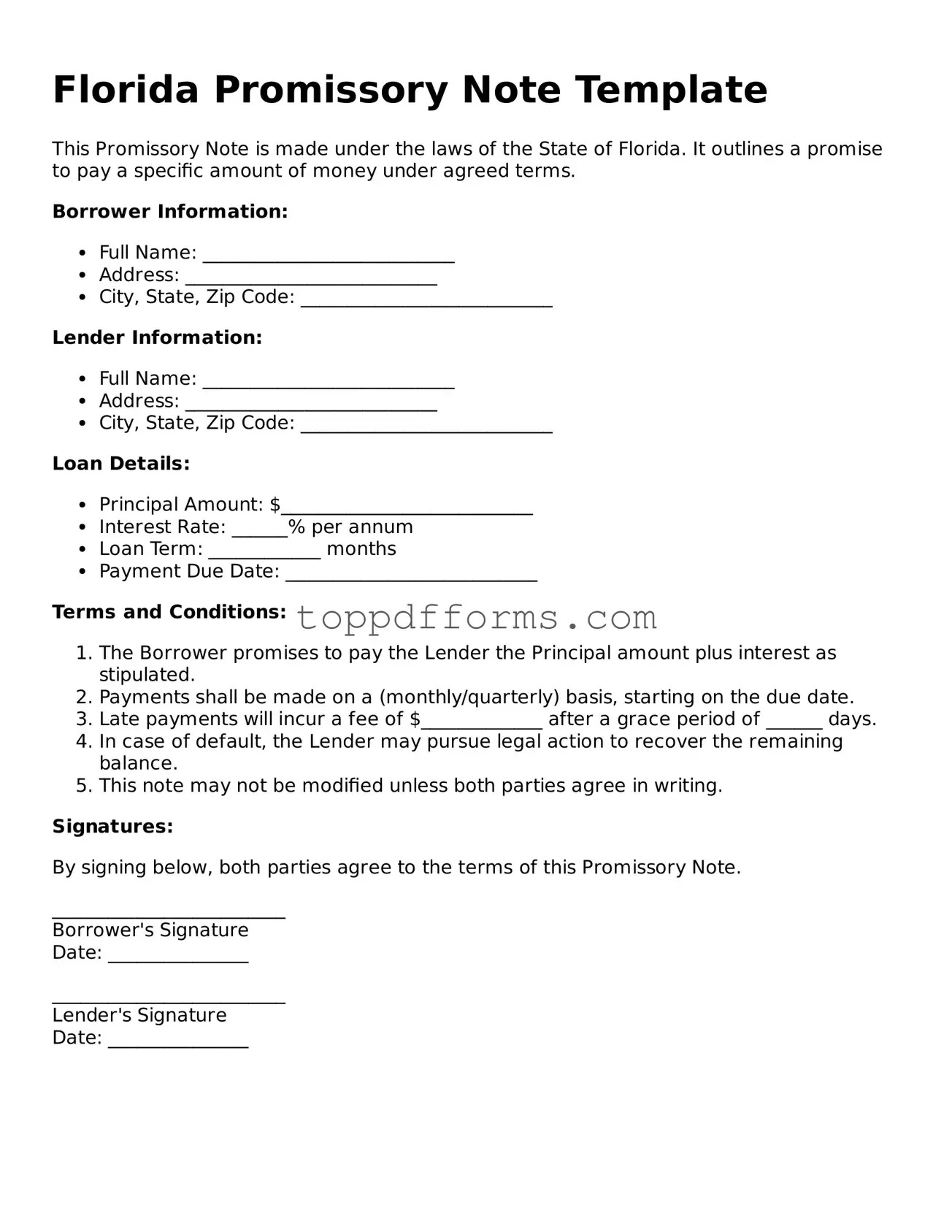

What is a Florida Promissory Note?

A Florida Promissory Note is a legal document that outlines a borrower's promise to repay a specified amount of money to a lender. This note includes details such as the loan amount, interest rate, repayment schedule, and any collateral securing the loan. It serves as evidence of the debt and establishes the terms of repayment.

Who can use a Florida Promissory Note?

Any individual or business can use a Florida Promissory Note. It is commonly utilized by lenders and borrowers in personal loans, business loans, or real estate transactions. Both parties must agree to the terms outlined in the note for it to be valid.

What are the essential components of a Florida Promissory Note?

A Florida Promissory Note typically includes the following components: the names and addresses of the borrower and lender, the principal amount of the loan, the interest rate, the repayment schedule, and any late fees or penalties. Additionally, it may specify the governing law and any provisions for default.

Is a Florida Promissory Note legally binding?

Yes, a Florida Promissory Note is a legally binding contract once signed by both parties. It obligates the borrower to repay the loan according to the agreed-upon terms. If the borrower defaults, the lender has the right to pursue legal action to recover the owed amount.

Can a Florida Promissory Note be modified?

Yes, a Florida Promissory Note can be modified if both parties agree to the changes. It is advisable to document any modifications in writing and have both parties sign the revised note to avoid potential disputes in the future.

What happens if the borrower defaults on the note?

If the borrower defaults on the Florida Promissory Note, the lender can take several actions. These may include charging late fees, accelerating the loan (demanding full repayment immediately), or initiating legal proceedings to recover the debt. The specific actions depend on the terms outlined in the note and applicable state laws.

Do I need a lawyer to create a Florida Promissory Note?

While it is not legally required to have a lawyer draft a Florida Promissory Note, consulting one can be beneficial. A lawyer can ensure that the document complies with state laws and adequately protects the interests of both parties. For simple loans, many templates are available that can be customized.

How is a Florida Promissory Note different from a loan agreement?

A Florida Promissory Note is a specific type of loan agreement that focuses primarily on the borrower's promise to repay the loan. In contrast, a loan agreement is a broader document that may include additional terms and conditions, such as covenants, representations, and warranties. Essentially, all promissory notes are loan agreements, but not all loan agreements are promissory notes.

Where can I find a Florida Promissory Note template?

Templates for Florida Promissory Notes can be found online through various legal document websites or state government resources. It is essential to select a template that complies with Florida law and meets the specific needs of the transaction. Customization may be necessary to reflect the unique terms of the loan.

PDF Overview

| Fact Name | Description |

|---|---|

| Definition | A Florida Promissory Note is a written promise to pay a specific amount of money to a designated person or entity at a specified time. |

| Governing Law | The Florida Promissory Note is governed by Florida Statutes, particularly Chapter 673, which deals with negotiable instruments. |

| Key Components | It typically includes the borrower's name, the lender's name, the loan amount, interest rate, repayment schedule, and any collateral involved. |

| Legal Enforceability | Once signed by both parties, the note is legally enforceable in a court of law, provided it meets all necessary requirements. |

Common mistakes

Filling out a Florida Promissory Note form can be straightforward, but several common mistakes can lead to complications. One frequent error is not including all necessary information. Borrowers must provide their name, address, and the amount borrowed. Omitting any of these details can render the note invalid.

Another common mistake involves incorrect dates. It is essential to accurately record the date the note is signed and the date the payment is due. If these dates are incorrect, it may create confusion regarding the timeline for repayment.

Many individuals also fail to specify the interest rate. A clear interest rate must be included to avoid disputes later. Without this detail, the note may be considered incomplete or unenforceable.

Some people overlook the importance of signatures. Both the borrower and the lender must sign the document for it to be legally binding. A missing signature can lead to significant issues down the line.

Another mistake is not clearly stating the payment terms. The note should outline whether payments are due monthly, quarterly, or in a lump sum. Vague terms can lead to misunderstandings about when and how much is owed.

Additionally, failing to include a default clause is a common oversight. This clause outlines what happens if the borrower fails to make payments. Without it, the lender may have limited options if the borrower defaults.

Lastly, neglecting to keep copies of the signed document can create problems. Both parties should retain a copy for their records. This ensures that everyone has access to the terms agreed upon, which can be crucial if disputes arise.

Other Common State-specific Promissory Note Forms

Georgia Promissory Note Template - This note outlines the repayment terms, including the principal amount, interest rates, and payment schedule.

Free Promissory Note Template Texas - Borrowers should carefully review the terms of a Promissory Note to ensure they align with their financial situation.

Create Promissory Note - This document can serve as evidence in legal situations if disputes arise over the loan.

To simplify the process of creating a comprehensive contract, you can access various resources like the PDF Templates that provide necessary formats and examples to assist you in drafting a legally binding Texas Vehicle Purchase Agreement.

Promissory Note Template California - Promissory notes are an integral part of personal and commercial finance practices.