Free IRS 1120 Form

Things You Should Know About This Form

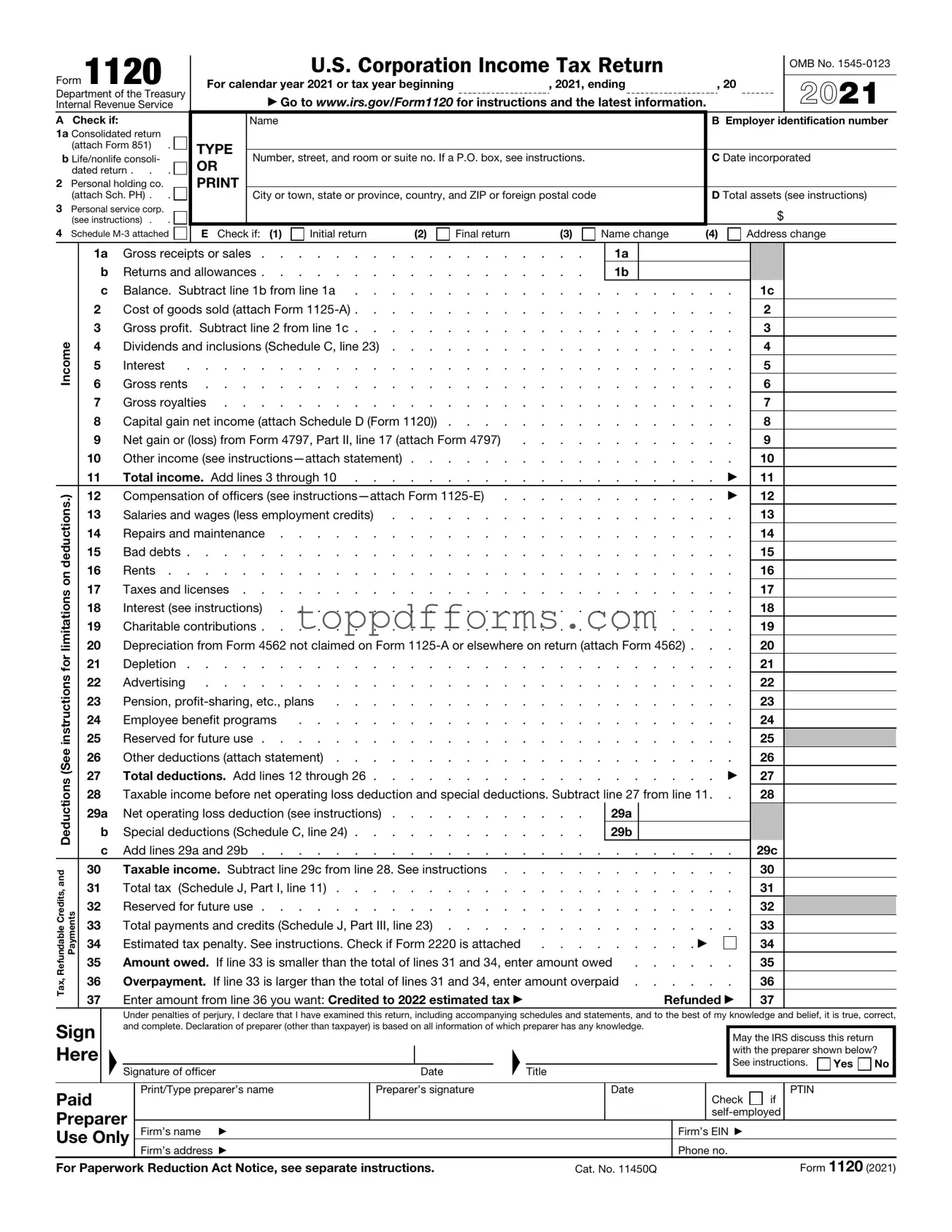

What is the IRS Form 1120?

IRS Form 1120 is the U.S. Corporation Income Tax Return. Corporations use this form to report their income, gains, losses, deductions, and credits. It is essential for any corporation to file this form annually, regardless of whether they owe taxes or not. By filing, corporations comply with federal tax laws and provide the IRS with necessary financial information.

Who needs to file Form 1120?

Any corporation that operates in the U.S. must file Form 1120. This includes C corporations, which are taxed separately from their owners. If your business is structured as a corporation, you are required to file this form, even if your corporation did not earn any income during the year. S corporations, however, file a different form, known as Form 1120S.

When is Form 1120 due?

Form 1120 is generally due on the 15th day of the fourth month after the end of your corporation's tax year. For corporations that operate on a calendar year, this means the due date is April 15. If the due date falls on a weekend or holiday, the deadline is extended to the next business day. Corporations can request a six-month extension to file, but this does not extend the time to pay any taxes owed.

What information do I need to complete Form 1120?

To complete Form 1120, you will need various financial information about your corporation. This includes total income, cost of goods sold, operating expenses, and any deductions or credits you plan to claim. You will also need to provide details about your corporation's assets, liabilities, and shareholders. Accurate records and documentation are crucial for filling out this form correctly.

File Information

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 1120 is used by corporations to report their income, gains, losses, deductions, and credits, as well as to calculate their federal income tax liability. |

| Filing Requirement | Corporations must file Form 1120 annually if they are subject to federal income tax. This includes both domestic and foreign corporations doing business in the U.S. |

| Due Date | The due date for filing Form 1120 is the 15th day of the fourth month after the end of the corporation's tax year. For corporations operating on a calendar year, this means April 15. |

| Extensions | Corporations can request an automatic six-month extension to file Form 1120 by submitting Form 7004 before the original due date. |

| State-Specific Forms | Many states have their own corporate income tax forms. For example, California requires Form 100, governed by the California Revenue and Taxation Code. |

| Tax Rates | The federal corporate tax rate is a flat 21% as of 2018, following the Tax Cuts and Jobs Act. This rate applies to taxable income. |

| Estimated Payments | Corporations may need to make estimated tax payments throughout the year if they expect to owe $500 or more in tax when filing Form 1120. |

| Schedule C | Form 1120 includes various schedules, such as Schedule C, which details the corporation's dividends, interest, and other income. |

| Penalties | Failure to file Form 1120 on time can result in penalties. The penalty is typically $210 for each month the return is late, up to a maximum of 12 months. |

Common mistakes

Filing the IRS Form 1120 can be a daunting task for many business owners. Mistakes can lead to delays, penalties, or even audits. Here are eight common mistakes that people often make when filling out this crucial form.

First, many individuals forget to include their Employer Identification Number (EIN). This number is essential for the IRS to identify your corporation. Without it, your form may be rejected or delayed. Always double-check that your EIN is correctly entered and matches the IRS records.

Another frequent error is misreporting income. Some businesses may overlook certain revenue streams or misclassify them. It's vital to report all sources of income accurately. Failing to do so can lead to discrepancies that raise red flags with the IRS.

Inaccurate deductions are also a common pitfall. Some filers might claim deductions they are not eligible for or miscalculate the amounts. It’s important to familiarize yourself with what qualifies as a deductible expense. Keeping thorough records throughout the year can help ensure accuracy when it’s time to file.

Many people neglect to sign and date the form. While it may seem minor, an unsigned form can be considered incomplete. Always remember to provide your signature and the date to validate your submission.

Another mistake involves incorrect calculations. Simple math errors can lead to significant issues. Take your time to double-check all figures or consider using tax software that can help minimize these mistakes.

Some filers fail to file on time, which can result in penalties and interest. Knowing the due date and planning ahead can help avoid this common error. If you need more time, consider filing for an extension rather than missing the deadline.

Inadequate documentation is also a mistake that can haunt you later. Supporting documents should be kept organized and accessible in case the IRS requests them. This includes receipts, invoices, and any other relevant records.

Lastly, many overlook the importance of consulting with a tax professional. While it may seem like an unnecessary expense, the expertise of a tax advisor can save you time and money in the long run. They can help navigate the complexities of the IRS Form 1120 and ensure everything is filed correctly.

By being aware of these common mistakes, you can approach your IRS Form 1120 with confidence. Taking the time to review your submission and seeking help when needed can make a significant difference in your filing experience.

Popular PDF Forms

How Much Does It Cost to Terminate Parental Rights in Texas - Awareness of this process ensures parents can act responsibly and with full knowledge of consequences.

For those seeking clarity in their vehicle transactions, the essential Motor Vehicle Bill of Sale documentation is crucial. This form not only facilitates the transfer of ownership but also serves as a legal safeguard for both parties involved. You can find more information regarding the process by visiting the detailed Motor Vehicle Bill of Sale guide.

How to Know If Im Having a Miscarriage - It emphasizes the compassionate side of medical practice during painful experiences.