Promissory Note Document for New York State

Things You Should Know About This Form

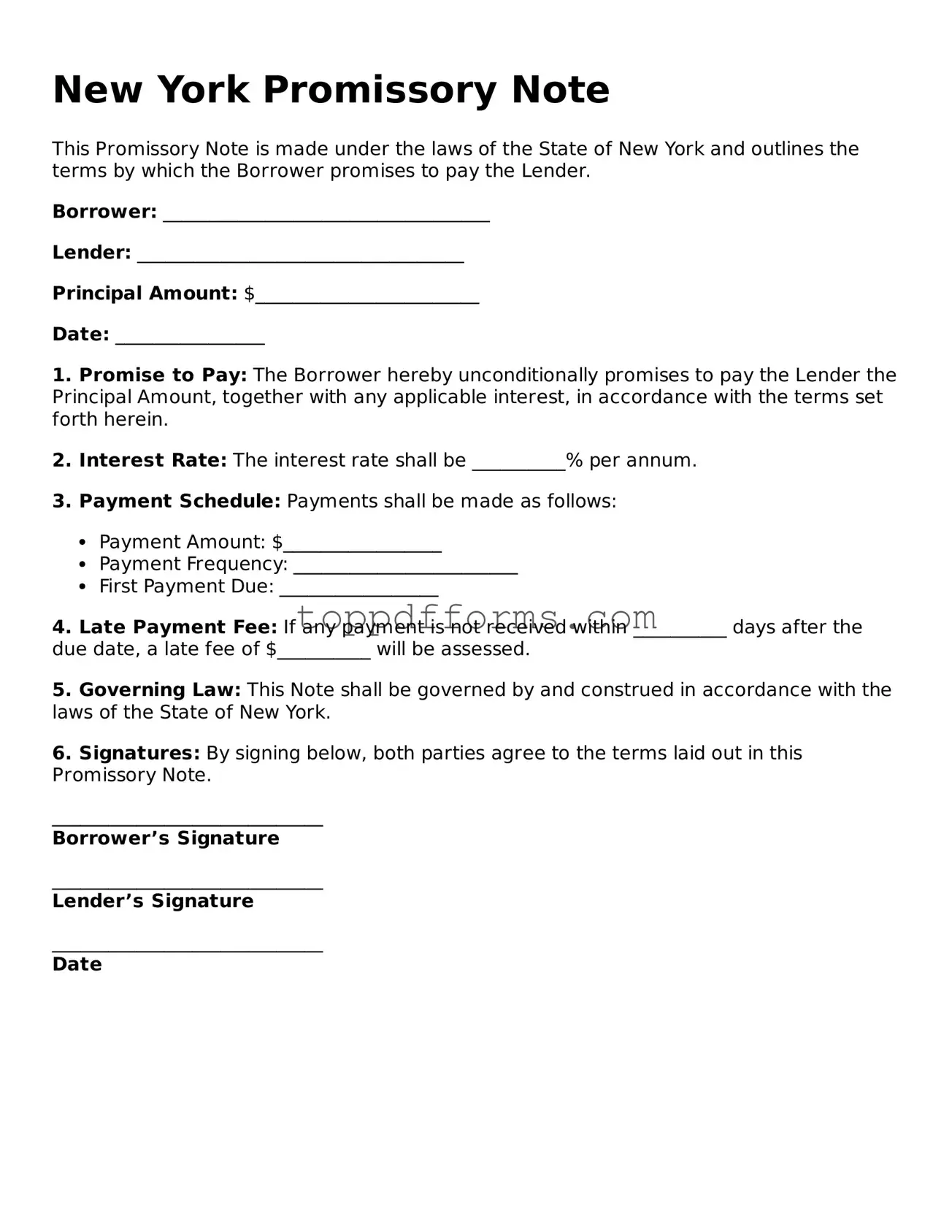

What is a New York Promissory Note?

A New York Promissory Note is a written agreement in which one party promises to pay a specific amount of money to another party at a predetermined time or on demand. This document serves as a legal record of the debt and outlines the terms of repayment, including interest rates and payment schedules.

Who typically uses a Promissory Note?

Individuals and businesses often use Promissory Notes. They are common in personal loans, business financing, and real estate transactions. Whether lending money to a friend or securing a loan for a business venture, a Promissory Note provides clarity and protection for both the lender and borrower.

What are the key components of a New York Promissory Note?

A typical Promissory Note includes the following components: the names and addresses of the parties involved, the principal amount borrowed, the interest rate, the repayment schedule, and any late fees or penalties. It may also specify whether the note is secured or unsecured, meaning whether collateral is involved.

Is a Promissory Note legally binding?

Yes, a properly executed Promissory Note is legally binding. Both parties must agree to the terms and sign the document. If one party fails to fulfill their obligations, the other party can take legal action to enforce the terms of the note.

Do I need a lawyer to create a Promissory Note?

While it is not required to have a lawyer draft a Promissory Note, consulting with one can be beneficial. A lawyer can ensure that the document meets all legal requirements and adequately protects your interests. However, many templates are available online for those who prefer to create one independently.

Can a Promissory Note be modified?

Yes, a Promissory Note can be modified if both parties agree to the changes. It’s essential to document any modifications in writing and have both parties sign the amended note. This helps avoid misunderstandings and ensures that the new terms are enforceable.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, meaning they fail to make payments as agreed, the lender has several options. They can pursue legal action to recover the owed amount, which may involve going to court. Additionally, if the note is secured, the lender may have the right to seize the collateral. It’s crucial to understand the terms outlined in the note regarding default and remedies.

PDF Overview

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated party at a defined time. |

| Governing Law | The New York Uniform Commercial Code (UCC) governs promissory notes in New York. |

| Parties Involved | The document involves at least two parties: the maker (borrower) and the payee (lender). |

| Requirements | The note must include the principal amount, interest rate, payment schedule, and maturity date. |

| Interest Rate | Interest can be fixed or variable, but it must be clearly stated in the document. |

| Signatures | The maker must sign the note for it to be valid; the payee's signature is not required. |

| Enforceability | A properly executed promissory note is legally enforceable in court. |

| Transferability | Promissory notes can be transferred to another party, often through endorsement. |

| Default Consequences | If the maker defaults, the payee may pursue legal action to recover the owed amount. |

| Notarization | While notarization is not required, it can provide additional legal protection for the parties involved. |

Common mistakes

When filling out a New York Promissory Note, individuals often make several common mistakes that can lead to confusion or legal issues down the line. Understanding these errors can help ensure that the document serves its intended purpose effectively. One significant mistake is failing to include all necessary parties. The note should clearly identify both the borrower and the lender. Omitting a party can create ambiguity about who is responsible for repayment.

Another frequent error is neglecting to specify the loan amount. While it may seem straightforward, leaving this detail out can lead to disputes later. A clear figure should be stated, along with any interest that may apply. This brings us to the next mistake: not detailing the interest rate. The Promissory Note should explicitly outline whether the interest is fixed or variable, and what the exact rate is. Without this information, the terms of repayment may become unclear.

People also often overlook the repayment schedule. It’s crucial to define when payments are due and how they should be made. Whether payments are to be made monthly, quarterly, or in a lump sum should be clearly articulated. Additionally, failing to include the consequences of late payments can lead to misunderstandings. The note should specify any penalties or fees that may apply if payments are not made on time.

Another common mistake involves not providing a clear description of the collateral, if any, backing the loan. If the loan is secured by an asset, that asset should be clearly identified in the note. This ensures that both parties understand the implications of default. Lastly, many individuals forget to sign the document. A Promissory Note is not valid unless it is signed by the borrower, and in some cases, the lender may also need to sign. This simple oversight can invalidate the entire agreement.

By being aware of these common mistakes, individuals can take steps to avoid them. A well-drafted Promissory Note protects both the lender and the borrower, ensuring clarity and reducing the potential for conflict. Taking the time to carefully fill out this form can save significant trouble in the future.

Other Common State-specific Promissory Note Forms

Online Promissory Note - A promissory note is typically straightforward, allowing parties to understand their responsibilities easily.

For anyone seeking to understand the legal implications of a Non-disclosure Agreement, this comprehensive guide will provide clarity on its role in protecting sensitive information during business dealings. To explore the specifics, visit our detailed resource on the Colorado Non-disclosure Agreement.

Promissory Note Template Florida - Specific clauses can detail the consequences of default, including remedies available to the lender.