Free Promissory Note Template

State-specific Guidelines for Promissory Note Documents

Promissory Note Form Categories

Things You Should Know About This Form

What is a Promissory Note?

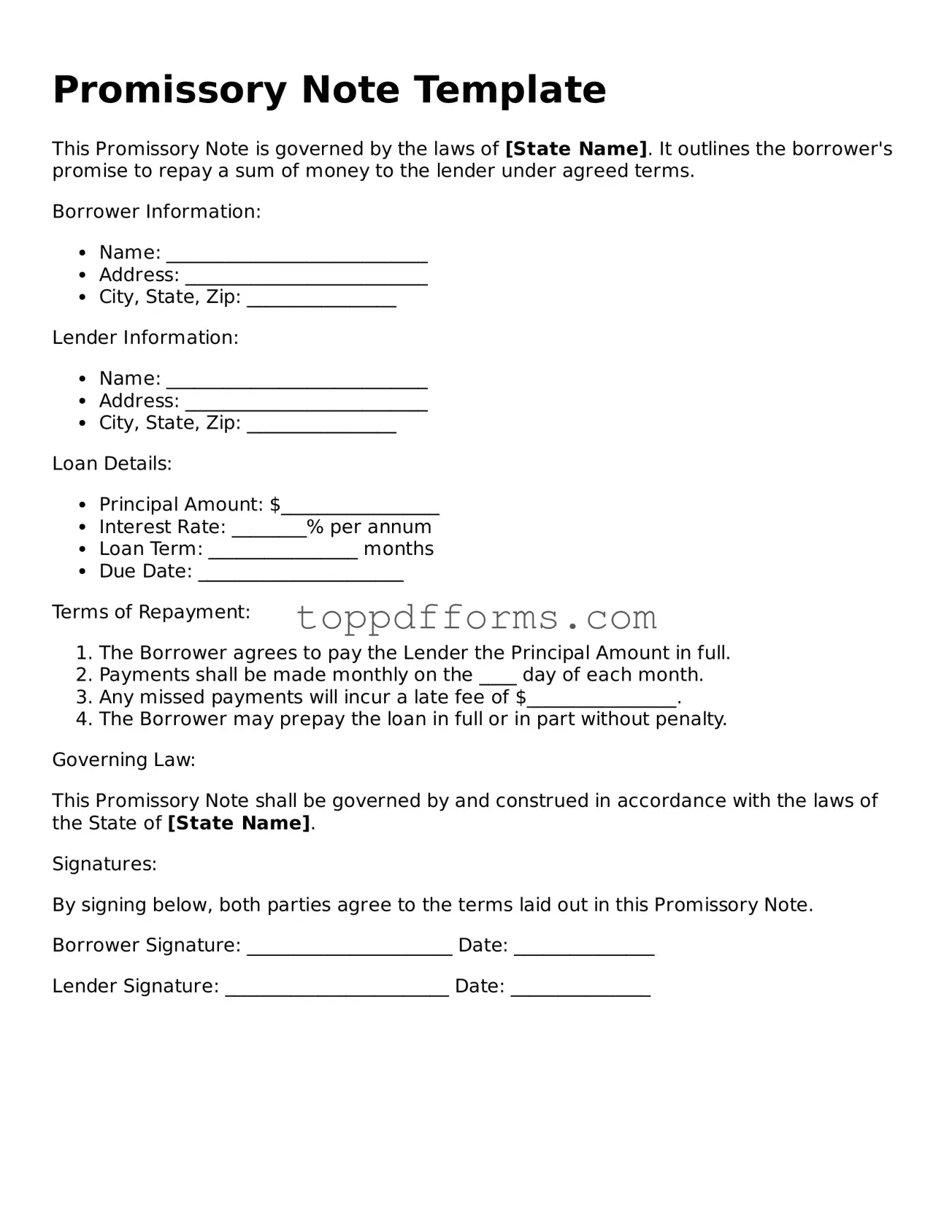

A promissory note is a written promise to pay a specific amount of money to a designated person or entity at a specified time or on demand. It outlines the terms of the loan, including the principal amount, interest rate, repayment schedule, and any penalties for late payments. This document serves as a legal agreement between the borrower and the lender, providing clarity and security for both parties involved in the transaction.

What information should be included in a Promissory Note?

A promissory note should include several key pieces of information. First, it should identify the borrower and lender, including their names and contact details. Next, it must specify the loan amount, interest rate, and repayment terms. Additionally, the note should outline any collateral securing the loan, if applicable. Finally, it is important to include a date and signatures from both parties to validate the agreement.

Is a Promissory Note legally binding?

Yes, a promissory note is legally binding as long as it meets certain requirements. Both parties must agree to the terms, and the document must be signed by the borrower. It is important to note that the enforceability of the note can depend on state laws and whether the terms are clear and fair. If disputes arise, the note can be presented in court as evidence of the agreement.

Can a Promissory Note be modified after it is signed?

Yes, a promissory note can be modified after it is signed, but both parties must agree to the changes. Any modifications should be documented in writing and signed by both the borrower and lender. This helps ensure that the new terms are clear and legally enforceable. It is advisable to keep a copy of the original note along with any amendments for record-keeping purposes.

PDF Overview

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a financial instrument that contains a written promise by one party to pay a specified sum of money to another party at a specified time. |

| Parties Involved | Typically, there are two parties involved: the maker (borrower) and the payee (lender). |

| Governing Law | In the United States, the Uniform Commercial Code (UCC) governs promissory notes, but specific state laws may also apply. |

| Interest Rate | Promissory notes can specify an interest rate, which may be fixed or variable, affecting the total amount to be repaid. |

| Default Consequences | If the maker defaults on the payment, the payee may have legal recourse, which can include pursuing collection or initiating foreclosure on collateral. |

| Transferability | Promissory notes are often transferable, meaning the payee can sell or assign the note to another party. |

Common mistakes

Filling out a Promissory Note form can be straightforward, but many people make common mistakes that can lead to complications later. One frequent error is failing to include all necessary details. A Promissory Note should clearly state the names of both the borrower and the lender. Omitting this information can create confusion and make the document unenforceable.

Another mistake involves incorrect or missing dates. The date when the note is signed is crucial, as it marks the beginning of the loan term. Leaving out the date or writing an incorrect one can lead to disputes over when payments are due. Always double-check the date to ensure accuracy.

Some individuals neglect to specify the interest rate. A Promissory Note should clearly state whether interest will be charged and, if so, what the rate will be. Failing to include this information can lead to misunderstandings and potential legal issues down the line.

Additionally, people sometimes overlook payment terms. It is essential to outline how and when payments will be made. This includes the payment schedule, the amount of each payment, and acceptable payment methods. Without clear terms, both parties may have different expectations, leading to conflict.

Another common error is not including a default clause. This clause outlines the consequences if the borrower fails to make payments as agreed. Without this provision, the lender may find it challenging to enforce their rights if the borrower defaults.

Some individuals forget to sign the document. A Promissory Note is not valid without the signatures of both parties. Ensure that both the borrower and lender sign the document to make it legally binding.

Finally, people often fail to keep copies of the signed Promissory Note. It is crucial for both parties to retain a copy for their records. This ensures that everyone has access to the same information regarding the loan terms and can refer back to it if needed.

Common Documents

What Is I-9 - This verification assists in assessing job stability.

Having a clear understanding of one's medical wishes is crucial, and individuals can obtain a Florida Do Not Resuscitate Order form to formalize their decisions. For detailed guidance on how to complete this form, visit floridaformspdf.com/printable-do-not-resuscitate-order-form, which provides the necessary resources and information to ensure that your preferences are properly documented and respected.

Designing a Family Crest - An imaginative crest celebrating diversity within lineage.

Non Renewal Lease Letter From Tenant - This notice may also serve to clarify any misunderstandings regarding lease terms and conditions.